I picked up Rich Dad Poor Dad on a coworker's recommendation during a period when I had $214 in savings and no idea why it never grew. I expected a lecture. Instead, I got a framework that explained, in plain terms, why everything I had been taught about money was designed to make someone else richer. The book is not perfect, and Kiyosaki is not shy about his opinions. But buried in the storytelling are ten ideas that most people genuinely were never told. These are the ones that stuck with me.

Rich Dad Poor Dad has sold over 40 million copies and consistently ranks as one of the top personal finance books on Amazon, with more than 107,000 reviews and a 4.7-star rating. That kind of staying power does not happen by accident. Something in it keeps resonating. Here is what that something is, broken into the ten lessons worth carrying with you.

Before we get into the lessons: the book costs less than a fast food lunch and takes a weekend to read.

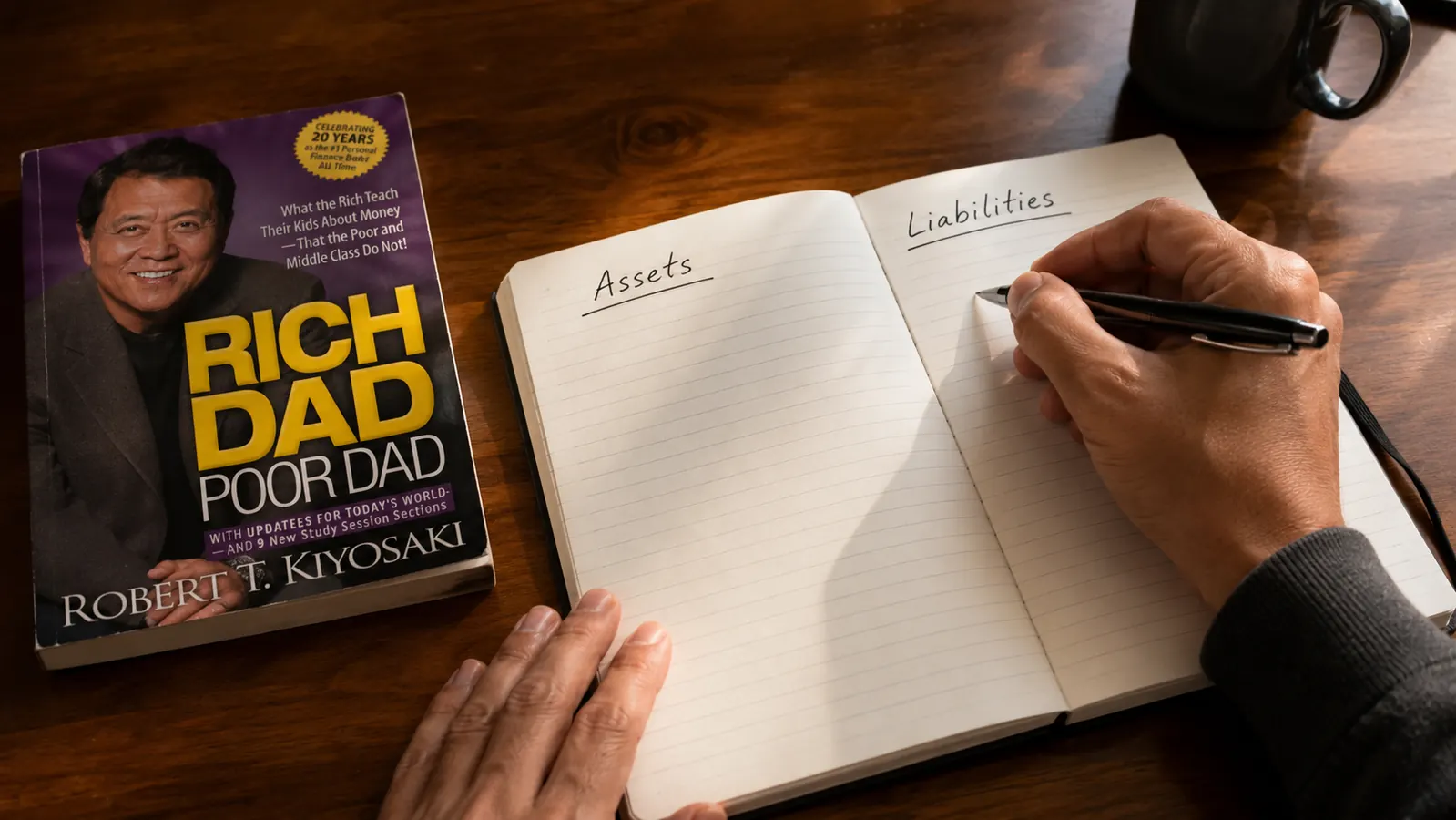

Rich Dad Poor Dad by Robert Kiyosaki is the starting point for most of these ideas. If you have not read it yet, it is worth having on hand while you go through this list.

Amazon Check Today's Price on Amazon →The Rich Do Not Work for Money. They Make Money Work for Them.

This is the opening premise of the book, and it sounds like a bumper sticker until you sit with it. Most of us trade time for dollars. When we stop working, the dollars stop coming. Kiyosaki's rich dad taught him to flip that relationship: set up income sources that run whether you show up or not. That is the long game the book keeps returning to. You do not have to start big. The point is to start thinking about it at all.

Financial Literacy Is Not Taught in School, and That Gap Is Expensive.

Kiyosaki spends a good chunk of the book pointing out that schools teach you how to be a good employee but almost nothing about how money actually works. Compound interest, balance sheets, cash flow, tax strategy, none of it. His argument is that this is not an accident. The system benefits from people who earn and spend without understanding the math underneath. Whether you agree with that read or not, the practical takeaway is real: you have to seek financial education yourself, because no one is going to hand it to you.

Know the Difference Between an Asset and a Liability.

This is the most cited idea in the book, and for good reason. Kiyosaki defines an asset as something that puts money in your pocket, and a liability as something that takes money out. By that standard, your house (while you are living in it and paying a mortgage) is a liability, not an asset. That idea made a lot of people angry in 2002 and still makes people defensive today. The point is not to never own a home. The point is to understand the cash flow direction of everything you buy before you buy it.

Mind Your Own Business. Your Employer's Business Is Not Yours.

Chapter three makes a distinction between your profession and your business. Your profession is how you pay the bills. Your business is your asset column: what you own, what you invest in, what generates income outside of your job. Kiyosaki's advice is to keep your day job but spend your spare time building your own asset column instead of spending every extra dollar on lifestyle upgrades. I had never thought about it that way before. It reframed what a 'good financial move' actually looked like on a Tuesday night.

The most important lesson Rich Dad Poor Dad taught me is that the financial rules most people follow were written by someone else, for someone else's benefit. Understanding that is worth more than the book costs.

Taxes Reward the Business Owner and Penalize the Employee.

Kiyosaki explains that employees are taxed before they spend, while business owners and investors can run many expenses through their business first and then pay taxes on what is left. This is not a loophole. It is how the tax code is written. He is not encouraging you to do anything illegal. He is encouraging you to understand the rules that already exist so you can use them. For a lot of readers, this chapter is the first time they realize the tax system is not neutral.

The Rich Invent Money. They Do Not Just Save It.

Saving is necessary, but Kiyosaki argues it is not sufficient and not what the wealthy primarily do. Wealthy people look for deals, negotiate, create equity, and spot opportunities that others miss because most people were never trained to look. He is not telling you to take reckless risks. He is telling you that financial intelligence is a skill that can be developed, and it pays better than simply depositing a fixed percentage every month and hoping the market cooperates.

Work to Learn, Not Just to Earn.

One of the most practical bits of advice in the book is to choose jobs that teach you valuable skills, not just jobs that pay the most right now. Kiyosaki says his rich dad encouraged him to take jobs specifically to learn sales, accounting, and how businesses operate, even at lower pay. That skill set compounds over a career in a way that a slightly higher starting salary does not. This is the kind of advice I wish someone had laid out for me at 22.

Overcome Fear and Self-Doubt, Because Those Are the Biggest Financial Obstacles.

Kiyosaki devotes real space to the emotional side of money, and it is not fluff. Fear of losing money keeps people in bad jobs. Self-doubt keeps people from learning new skills. Cynicism keeps people from even trying. He frames these as habits you can identify and interrupt, not permanent character traits. I appreciated that he did not pretend the mental side is easy. He just made the case that it is worth addressing directly, because no financial strategy works if you are too scared to execute it.

Pay Yourself First, Even When It Is Hard.

This phrase gets thrown around so often that it has almost lost meaning. But in context, Kiyosaki explains it differently than most people do. He is not just saying to automate your savings before you spend. He is saying to use the pressure of slightly tight finances as motivation to find additional income or cut costs creatively, rather than simply skipping the contribution. Pay yourself first, then figure out the rest. The discomfort, he argues, is what generates ingenuity. It is a different framing than most budgeting advice takes.

Take Action. An Imperfect Plan Started Now Beats a Perfect Plan Started Never.

The final lesson the book hammers on is motion. Kiyosaki is not patient with people who say they will start investing once they know more, or once conditions improve, or once the kids are through school. He calls that pattern 'analysis paralysis' and spends the last section of the book pushing readers to take small, concrete steps now, learn from the results, and adjust. It is the lesson I find the most practically useful, because it is the one that can be applied today with no additional information or resources.

What I Would Skip in the Book

The book is not without its problems. Kiyosaki's investment examples are heavy on real estate, which is not accessible to everyone and not the only path. Some of the storytelling is vague, and critics have pointed out that his 'rich dad' character may be more parable than biography. A few of the specific financial claims are dated or oversimplified. You would not want to use this book as your only financial reference. But as a starting framework, as a way to shift how you think about the relationship between your time, your money, and your future, it holds up better than most books in this category.

Read it for the mindset shift, not the specific investment playbook. The mindset is where the real value lives.

If even three of these ten ideas are new to you, the book is worth reading cover to cover.

Rich Dad Poor Dad by Robert Kiyosaki is one of the most-reviewed personal finance books on Amazon, with a 4.7-star rating across more than 107,000 reviews. It is a fast read and a genuine starting point for understanding money differently.

Amazon Check Today's Price on Amazon →