My name is Carla. I am 34, I work as a medical office scheduler in Columbus, Ohio, and for most of my adult life my budgeting strategy was checking my bank balance before I swiped my card and hoping for the best. I tried Mint. I tried a color-coded spreadsheet I found on Pinterest. I downloaded YNAB and used it for exactly eleven days before I stopped opening the app. Nothing stuck. Then in October, my coworker Lisa pulled a navy blue binder out of her bag at lunch and said, 'This is the only thing that has ever worked for me.' That binder was the SKYDUE Budget Binder. I ordered one that same afternoon. Six months later, I am writing this review not because everything is magically fixed, but because something real has changed.

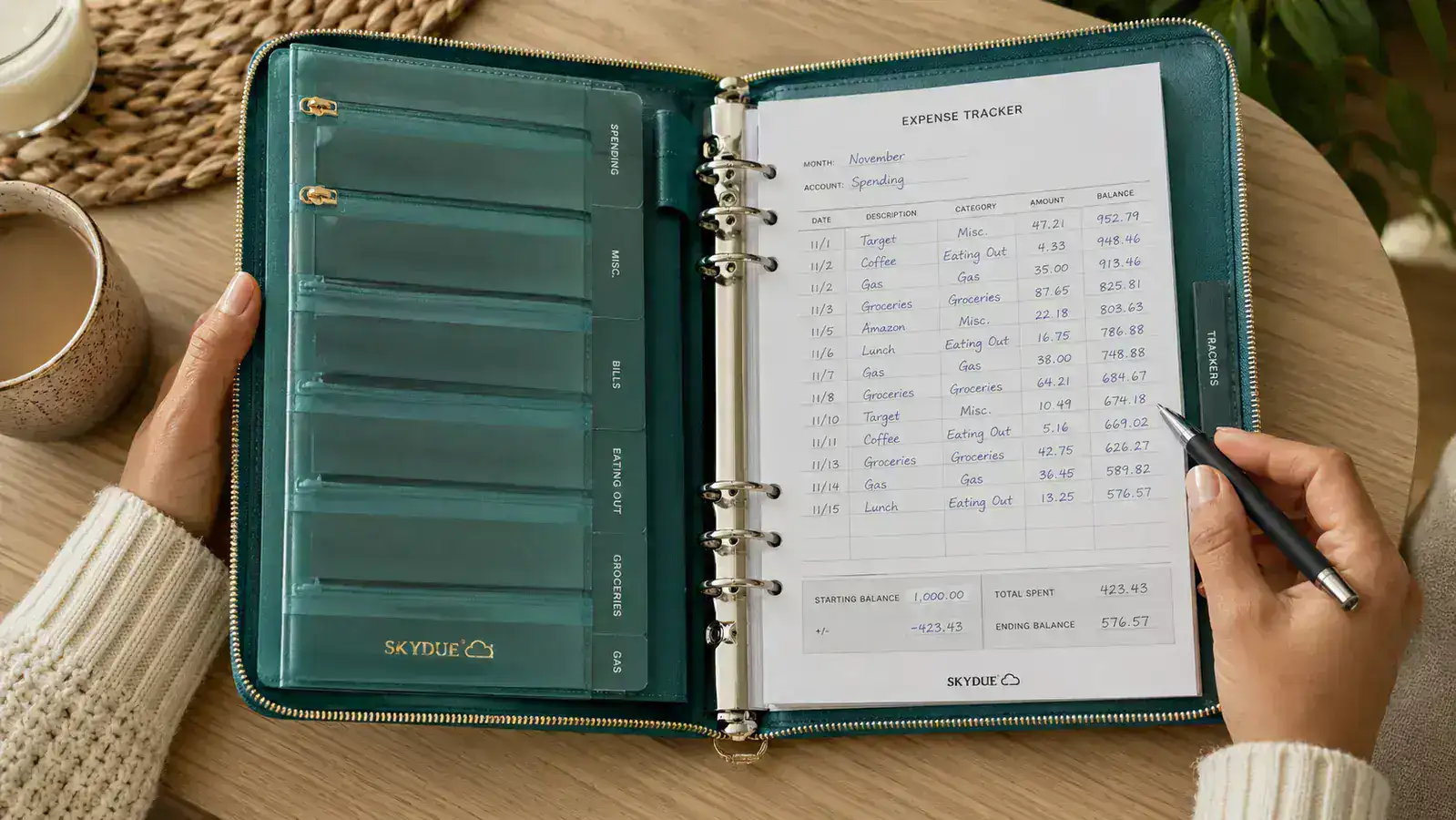

The SKYDUE Budget Binder is a physical cash-envelope budgeting system. It comes with a zippered binder, a set of clear plastic zipper pouches, printed label stickers for your spending categories, and expense tracking sheets you fill in by hand. The idea is old-fashioned on purpose: you withdraw your paycheck in cash, divide it into labeled envelopes by category, and when the envelope is empty, spending in that category is done for the month. No app, no password, no screen. Just cash in a pouch and the discipline to stop when it runs out.

The Quick Verdict

The SKYDUE binder is the most effective low-tech budgeting tool I have found for people who have tried apps and failed. It is not perfect, but it is the first thing that made my grocery and dining-out spending feel controllable in years.

Amazon Check Today's Price →Still losing track of where your paycheck goes every month? The SKYDUE Binder gives you a physical system that makes overspending harder than not overspending.

Over 19,000 buyers have rated it 4.7 stars. Check today's price on Amazon and see if it is the missing piece your budget needs.

Amazon Check Today's Price on Amazon →How I Set It Up and How I Have Used It

When the binder arrived, my first impression was that it felt sturdier than I expected for the price. The zipper pouches are clear plastic, thick enough that they do not tear when you stuff them with folded twenties. The binder itself has a snap closure and a carry handle, so it does not feel flimsy. Setup took me about an hour the first time. I labeled eight envelopes: Groceries, Gas, Dining Out, Household Supplies, Personal Care, Entertainment, Kids' Activities, and a Misc. Catch-All. I used the printed label stickers that came in the pack, though I later switched to my own handwritten labels because I wanted to reorganize my categories after month two.

My pay period is biweekly. On the first and fifteenth of each month, I go to the ATM and pull out the cash I have budgeted for each category. Then I sit at the kitchen table, which takes me about twenty minutes, and divide the bills into the envelopes while I fill in the starting balance on the tracking sheet. That tracking sheet is inside the binder too: a simple printed grid where you log what you spent, where, and how much is left. I do not love filling it in every single time I spend money, so I do a nightly five-minute recap instead. It is not perfect, but it is honest.

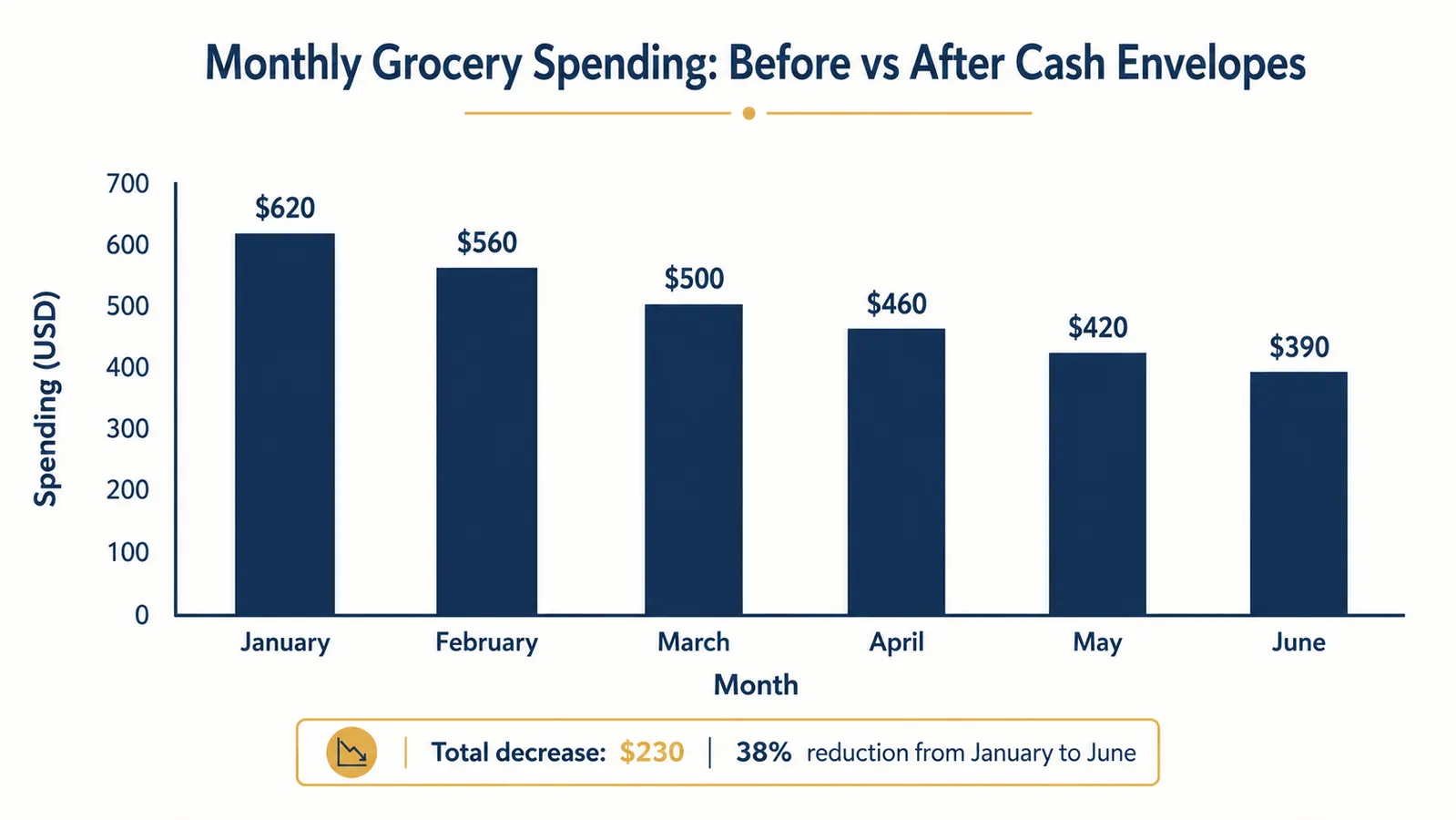

The first month was uncomfortable. I ran out of grocery money on the 24th and had to get creative with what was in the freezer for the last week of the month. That was frustrating in the moment. But I also spent $390 on groceries that month, compared to the $580 I had spent the month before when I was not tracking anything. The discomfort was the system working.

What the Binder Includes and What It Does Not

The SKYDUE Budget Binder ships with the zippered A6-size binder, six clear zipper pouches in two sizes, a set of preprinted category sticker labels (Groceries, Gas, Entertainment, Bills, Savings, and a few others), monthly budget summary sheets, and daily/weekly expense log sheets. You can also buy refill packs of the expense sheets separately on Amazon, which I did around month three when I ran out.

What it does not include: any kind of debt tracker, savings goal worksheet, or monthly income calculation page. If you want to use the binder for your full financial picture, you will need to either buy a companion budget workbook or use your own notebook alongside it. I keep a simple spiral notebook where I track my credit card balance and my emergency fund balance separately. The SKYDUE binder handles my cash spending categories. My fixed bills like rent, utilities, and insurance stay on autopay and are not in the envelopes at all.

One thing worth noting: the binder is sized for A6 papers, which are smaller than a standard letter sheet. The included expense sheets fit perfectly. If you try to tuck in a full-size piece of paper or a printed spreadsheet, it will not fit without folding. That is not a flaw, but it is something to know going in.

Six Months of Real Numbers

I tracked my spending in the three main categories I had always overspent in: Groceries, Dining Out, and Miscellaneous. Here is what the six-month arc looked like for me. In October, my first month with the binder, my grocery envelope was $400 and I went over by $23 before I got the hang of it. By December, I came in $18 under and moved that surplus into my Misc. envelope. By March, I had found a rhythm where I consistently came in under budget in Groceries by $30 to $50, and I started rolling that money into a small savings envelope I added to the binder. At the end of six months, that savings envelope had $247 in it from grocery and entertainment underspend. Not life-changing. But it was the first time I had accumulated any discretionary savings that I had not immediately spent on something.

My Dining Out category showed the most dramatic change. Before the binder, I was spending somewhere between $200 and $350 a month eating out, depending on the month, with no real awareness of where it was landing. The physical envelope forced a decision: I set my Dining Out budget at $120 a month. The first two months, I hit the limit around the 18th of the month and had to say no to coworker lunch invites. By month four, I had adjusted my habits without much conscious effort. I started meal-prepping on Sundays more consistently because going out felt wasteful when I could see the envelope thinning out.

The first month I ran out of grocery money on the 24th. That was uncomfortable. It was also the month I spent $190 less than the month before.

Build Quality and Daily Use Over Six Months

After six months of weekly use, the binder is still in good shape. The snap closure still snaps cleanly. Two of the zipper pouches have minor scuff marks but no tears. The binder cover has some wear on the corners. For the price, the durability is better than I expected. I have seen some reviewers on Amazon complain that the pouches feel cheap; mine have held up fine, but I also do not stuff them until they are overfull. If you are the kind of person who jams everything in and yanks it closed, you might have a different experience.

Day to day, the binder lives on my kitchen counter in a small basket. I grab it when I leave for grocery shopping the same way I grab my keys. It has become a habit item rather than a chore item, which I think is the real reason cash envelope budgeting works when apps do not. The physical friction of handling cash is the point. Swiping a card feels like nothing. Counting out forty dollars from an envelope and watching the balance drop feels like something.

Where the SKYDUE Binder Falls Short

Let me be honest about the friction points. Carrying cash is not convenient in 2026. My gym membership, my Netflix, my phone bill, and most of my kids' school-related payments are all digital. Cash envelopes only help with the categories where you can actually pay in cash, and that list is shorter than it used to be. Groceries, gas, and dining out are the main ones that still work. Anything subscription-based or paid online stays off the system entirely.

The expense tracking sheets also require a level of consistency that is easy to let slide. When I am tired or busy, I skip the nightly log and try to remember what I spent two days later. That introduces errors. If you are not willing to track spending regularly, the binder still provides some control (the envelope runs out when it runs out), but you lose the insight into your spending patterns that the tracking sheets are supposed to give you.

There is also the safety question. Carrying around $400 to $600 in cash for the month makes some people uncomfortable, and reasonably so. I keep most of my cash at home and only carry the envelope I need for a specific shopping trip. That works for me, but it requires a little planning.

What I Liked

- Physical envelopes create real spending friction that digital budgets cannot replicate

- Durable construction that has held up through six months of regular use

- Includes expense tracking sheets, labels, and two envelope sizes out of the box

- Extremely low cost for a tool that actually changes spending behavior

- No app, subscription, or screen required

- Forces a monthly budget conversation with yourself on payday

Where It Falls Short

- Only effective for cash-payable categories like groceries, gas, and dining out

- Expense tracking sheets require consistent daily or nightly habit

- Does not include debt tracking, savings goal sheets, or income calculation pages

- Carrying cash for multiple categories requires planning and some comfort with physical money

- Refill expense sheets need to be purchased separately after a few months

How It Compares to Apps and Spreadsheets

I want to address the obvious question: why use a physical binder when YNAB, Mint, and a dozen other apps exist? I tried those apps. My experience, and the experience I hear from a lot of people, is that digital budgets are too easy to ignore. You can open an app, see that you are $80 over in Dining Out, close the app, and still go get sushi on Friday. The number on the screen does not stop you. An empty envelope stops you.

That said, apps are better for tracking fixed expenses, subscriptions, and bills. They sync automatically and give you a whole-picture view of your finances that the binder cannot match. My honest take is that the binder is not a replacement for a budgeting app. It is a replacement for willpower in the specific categories where willpower keeps failing you. If you have been struggling with overspending on groceries and eating out for years, this binder will do more for you in 30 days than most apps will do in a year. If you need to track 25 spending categories including digital subscriptions and automatic transfers, you will need a different tool alongside it. I cover that comparison in more detail in my piece on the SKYDUE Binder vs YNAB.

Who This Is For

The SKYDUE Budget Binder is the right tool if you have tried budgeting apps more than once and abandoned them within a month. It is right for you if you know intellectually how much you should spend on groceries but you keep going over anyway. It is right for you if you want to start a cash-based envelope system and do not want to build one from scratch using random envelopes and a notebook. It is right for you if you are living paycheck to paycheck and the main problem is not that you do not earn enough, but that you are not sure where the money goes. At its price point, the downside of trying it is low. You can know within one month whether the physical system clicks for you. Most people know within two weeks. If you want to understand more about why the envelope method works for so many people, I have a longer piece on the 10 reasons the cash envelope system works that goes into the psychology behind it.

Who Should Skip It

Skip the binder if almost all of your spending is digital and you cannot realistically pay for your main spending categories in cash. If you live in a city where you tap your phone for everything, carry a card for transit, and order groceries for delivery, the envelope system will feel like trying to solve a problem with the wrong tool. Skip it also if you need to track your full financial picture including investments, credit card payoffs, and debt repayment all in one place. The binder tracks cash categories only. It is a piece of a financial system, not the whole thing. And if you have been doing envelope budgeting for more than a year already with good results, you have probably outgrown the need for a starter binder and can move to a more advanced tracking method.

If digital budgeting has failed you more than once, the SKYDUE Binder is worth a try. The cash is the accountability. The binder is just the structure around it.

Rated 4.7 stars by more than 19,000 people. Check today's price on Amazon and see if it fits your budget categories.

Amazon Check Today's Price on Amazon →