I picked up Rich Dad Poor Dad for the first time on a Tuesday night after another month of running out of money three days before payday. I was 34, had about $400 in savings, and had been telling myself I would start investing someday for going on four years. What I expected from the book was motivational fluff. What I got instead was a framework for thinking about money that genuinely changed how I made decisions. Not overnight, not dramatically, but steadily. That is the word I keep coming back to: steadily.

This guide is not about getting rich fast. It is about applying what Robert Kiyosaki actually teaches in Rich Dad Poor Dad when you are starting from a real zero: no investment account, maybe some debt, and a paycheck that feels like it disappears before you finish spending it. There is a sequence to this that most people miss because they skip ahead, so I am going to walk through it in the order that actually works.

Start where Rich Dad started: with the book itself.

Rich Dad Poor Dad has over 107,000 reviews on Amazon and has been in print for more than 25 years. It is still the clearest explanation of the asset-versus-liability distinction that most people were never taught. Reading it before you do anything else is Step 0.

Amazon Check Today's Price on Amazon →Step 1: Learn the Asset and Liability Distinction Before You Move Any Money

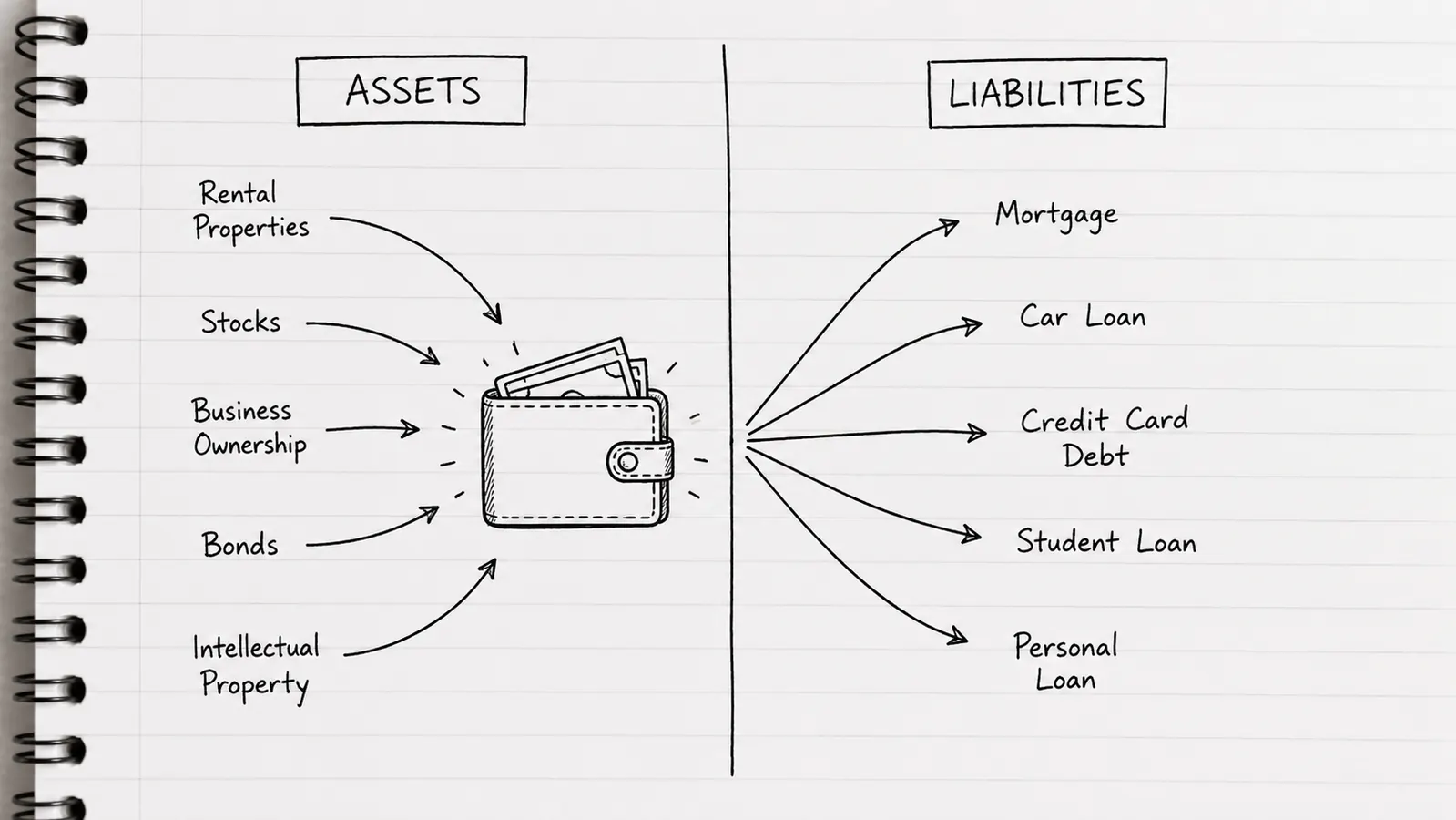

The single most important idea in Rich Dad Poor Dad is one your financial advisor probably never drew out for you: assets put money into your pocket, and liabilities take money out. That sounds almost too simple, but Kiyosaki's real point is that most people think their car and their house are assets. They are not. They are liabilities. Your car costs you insurance, gas, and maintenance every month. Your mortgage, if the house is not generating rental income, takes money out every month. Knowing this changes how you look at every purchase.

Before you touch a brokerage account or think about real estate, sit down with a piece of paper and write out two columns: what you own that puts money in, and what you own that takes money out. Be brutally honest. Most people starting from zero will find the asset column is empty and the liability column has a car payment, maybe credit card balances, and a phone plan. That is okay. The point of this step is not to feel bad. It is to see clearly. You cannot fix what you have not named.

Rich Dad Poor Dad is where this mental model comes from, and reading it first gives you the vocabulary for every step that follows. If you have not read it yet, that is your actual first move. Kiyosaki explains the concept across the first several chapters in plain enough language that you do not need any financial background to follow it.

Step 2: Build Financial Literacy So You Can Read the Scoreboard

Kiyosaki is emphatic about something most people skip: you need to understand how money works before you start moving it around. Financial literacy, in the Rich Dad framework, means being able to read an income statement and a balance sheet. Not at an accounting level. At a personal level. Income comes in. Expenses go out. What remains is what you have available to buy assets with. That is the whole game.

In practical terms this means knowing your real numbers: your monthly take-home pay, your fixed expenses, your variable expenses, and what is left. Most people have a rough sense but have never actually added it up. I had not. When I did it for the first time, I found I was spending about $210 a month on subscriptions I had signed up for and mostly forgotten. That money was just gone every month. It was not going toward anything that put money back in.

Financial literacy also means understanding the difference between earned income, portfolio income, and passive income. Kiyosaki's Rich Dad framework is largely built around moving from earning all your income from labor toward having income that comes from assets you own. You do not get there in month one. But understanding the destination changes the decisions you make along the way. Read the book with a notepad. Write down the terms you want to understand better. Look them up. That is the literacy-building work.

The Rich Dad framework is not about earning more. It is about directing what you already earn differently. Once that clicked for me, even small amounts of money started to feel like they had a job to do.

Step 3: Control Spending by Paying Yourself First

Pay yourself first is one of the oldest ideas in personal finance and Rich Dad Poor Dad returns to it repeatedly. The concept is simple: before you pay any bill, before you spend anything, set aside a percentage of your income for acquiring assets. Not after. Not with what is left over. First. Kiyosaki argues that most people do it backwards: they pay everyone else and save whatever is left, which is usually nothing.

When I started doing this I did not have a lot to work with. I set aside $75 from every paycheck before anything else touched it. That went into a separate savings account I did not have a debit card for. Was it enough to change my life immediately? No. But it built a habit and it built a small buffer that stopped me from reaching for my credit card every time an unexpected expense came up. Within about five months I had around $900 sitting there, which was more savings than I had held in years.

Controlling spending does not mean depriving yourself of everything you enjoy. It means having a clear, honest conversation with your budget about what is actually going toward building something and what is just leaking out. The Rich Dad framework calls this making your money work for you rather than working for your money. The first practical expression of that is keeping some of what you earn long enough to deploy it toward something that will give it back.

Step 4: Buy or Build Your First Income-Producing Asset

This is the step most people want to jump to first. Kiyosaki is very clear that it should come after you have done the earlier work: understood the asset-liability distinction, gotten financially literate enough to read your own numbers, and started paying yourself first. When you have done those three things, even if your initial amount is small, you are ready to buy your first real asset.

For most people starting from zero, the most accessible first asset is an index fund in a tax-advantaged account like a Roth IRA or a 401k with an employer match. Kiyosaki himself focuses on real estate and business ownership in the book, and those are valid longer-term paths. But for someone with $500 in savings and a regular paycheck, a low-cost index fund is the realistic starting point. It is an asset in the technical sense: it holds value and, over time, pays you in the form of dividends and capital appreciation. If you want to go deeper on index funds, our piece on the Little Book of Common Sense Investing covers that in more detail.

The key thing Kiyosaki is pointing at is not a specific vehicle. It is a habit of mind: every dollar you earn should be evaluated through the question of whether it is buying you something that generates income or taking money away from your ability to do that. When you buy a $12 book that teaches you how to earn more, that is an asset. When you pay down a high-interest credit card, you are eliminating a liability that was costing you money every month. Both of those are the Rich Dad move. The question to ask yourself is whether the thing you are about to do with your money is adding to the asset column or the liability column.

Step 5: Reinvest Returns and Repeat the Cycle

This is where the Rich Dad framework becomes self-reinforcing, and it is also where most people who start building wealth quietly stay consistent and stop looking for shortcuts. Once you have an asset that is generating anything, even a small amount, the single most powerful move is to put that return back into acquiring more assets rather than spending it.

Compounding is not exciting to talk about. It does not make for a dramatic social media post. But it is the actual mechanism behind how modest investors accumulate real financial stability over time. A Roth IRA with consistent monthly contributions and dividends reinvested does something remarkable over fifteen or twenty years that a savings account never will. Kiyosaki's framework is built around the idea that the rich do not work for money in the conventional sense. They work once to understand a system, then set up assets that keep working while they do other things.

In practice, reinvesting looks like this: you get a $40 dividend in your index fund account. You do not withdraw it. You let it buy more shares. Next quarter those shares pay a little dividend too. Over years, this quietly adds up. The same applies if you eventually move into other assets like rental property: the rent pays the mortgage and some amount of profit, and that profit gets directed toward another asset rather than toward lifestyle inflation. The Rich Dad framework does not require a dramatic income to work. It requires a different relationship with whatever income you already have.

What Else Helps

Rich Dad Poor Dad is a mindset book more than a step-by-step manual. It gives you the framework and the vocabulary, but it does not tell you exactly which brokerage to open or how to read a tax form. That is by design: Kiyosaki is trying to shift how you think, not write a technical how-to. Once you finish it, there are a few practical companions worth having.

For investing mechanics, something like John Bogle's work on index funds translates the Rich Dad asset-buying concept into a concrete, low-cost vehicle that does not require you to be a stock picker. Our review of the Little Book of Common Sense Investing goes deeper on why that approach holds up over time and how to get started with it. For budgeting and tracking, a physical system like a cash envelope binder can make the pay-yourself-first habit feel real in a way that apps sometimes do not, especially in the early months when you are still building the behavior.

Rich Dad Poor Dad also has a companion community and a board game called Cashflow that Kiyosaki designed specifically to teach the asset-versus-liability concept through repeated play. Some people find that game clicks the lesson into place faster than the book alone. It is worth knowing it exists. None of these are required. The book itself is where you start, and for most people it is where the shift happens.

The framework starts with the book. Everything else builds from there.

Rich Dad Poor Dad is the most widely read personal finance book of the past 25 years for a reason. If you are starting from zero and want a framework for thinking about money that goes beyond budgeting advice, this is the place to start. It is also one of the most honest books about the difference between how the wealthy think and how most people were taught to think.

Amazon Check Today's Price on Amazon →