If you have credit card balances, a car loan, medical bills, and maybe a student loan or two, you already know the feeling: every paycheck leaves and you are not sure what it actually paid down. You make the minimum payments, the balances barely move, and six months later you are in the same spot. That cycle is the problem the Total Money Makeover by Dave Ramsey was written to break. It has helped over five million people get out of debt, and the core method is not complicated. But most people who buy the book never finish the first step because they do not have a clear picture of what to actually do in week one.

This guide walks through each step of the Total Money Makeover system in plain language. Not a summary of the book, and not a lecture. A walkthrough of what you actually do, in order, starting from wherever you are right now. I went through this process myself starting in early 2024 with just under $14,000 in non-mortgage debt spread across a store card, two credit cards, and a personal loan. By the end of that year, three of the four were gone. Here is what worked.

Stuck in the minimum-payment loop? This is the book that breaks it.

The Total Money Makeover lays out Dave Ramsey's complete Baby Steps system in one place. Over 22,000 Amazon reviewers give it 4.7 stars. It is worth having the physical book so you can mark it up, highlight it, and come back to it on the weeks when motivation is low.

Amazon Check Today's Price on Amazon →Step 1: Write Down Every Debt You Owe in One Place

Before you touch a dollar, you need a complete list. Not in your head. On paper or in a spreadsheet, somewhere you can see it all at once. For each debt, write the creditor name, the current balance, the minimum monthly payment, and the interest rate. Do not skip any of them. Include the medical bill from two years ago, the store card you forgot about, the money you owe a family member. Everything. If you are not sure of the exact balance on something, log in and check. Estimates will not give you a real number to work with.

When I did this the first time, I had been avoiding the exact total for months. Seeing it written out as $13,840 was uncomfortable, but it was also clarifying. It stopped being a vague cloud of stress and became a specific number I could make a plan around. The Total Money Makeover calls this getting out of denial, and that is exactly what it is. You cannot attack something you refuse to look at directly.

Once your list is complete, sort your debts from smallest balance to largest balance. Set the interest rates to the side for now. Ramsey's system ignores interest rate order on purpose, and there is a real behavioral reason for that, which the next step explains.

Step 2: Build a Small Emergency Fund First (Baby Step 1)

Here is where a lot of people skip ahead and end up back at square one. Before you pay down a single debt beyond the minimum, you need $1,000 in a savings account set aside as a starter emergency fund. Not invested. Just sitting there as cash. The Total Money Makeover calls this Baby Step 1, and it is not optional. The reason is simple: if you throw everything at debt and then your car needs a $700 repair, you go right back to the credit card. The $1,000 is not a goal. It is protection so one emergency does not blow up your momentum.

If you have more than $1,000 already in savings, leave $1,000 there and redirect the rest toward your debt list. If you have less, focus on reaching that $1,000 mark before doing anything else. Sell something, pick up a weekend shift, pause a subscription or two temporarily. Whatever it takes to get that cushion in place. One month of focused effort is usually enough to get there, even on a tight income.

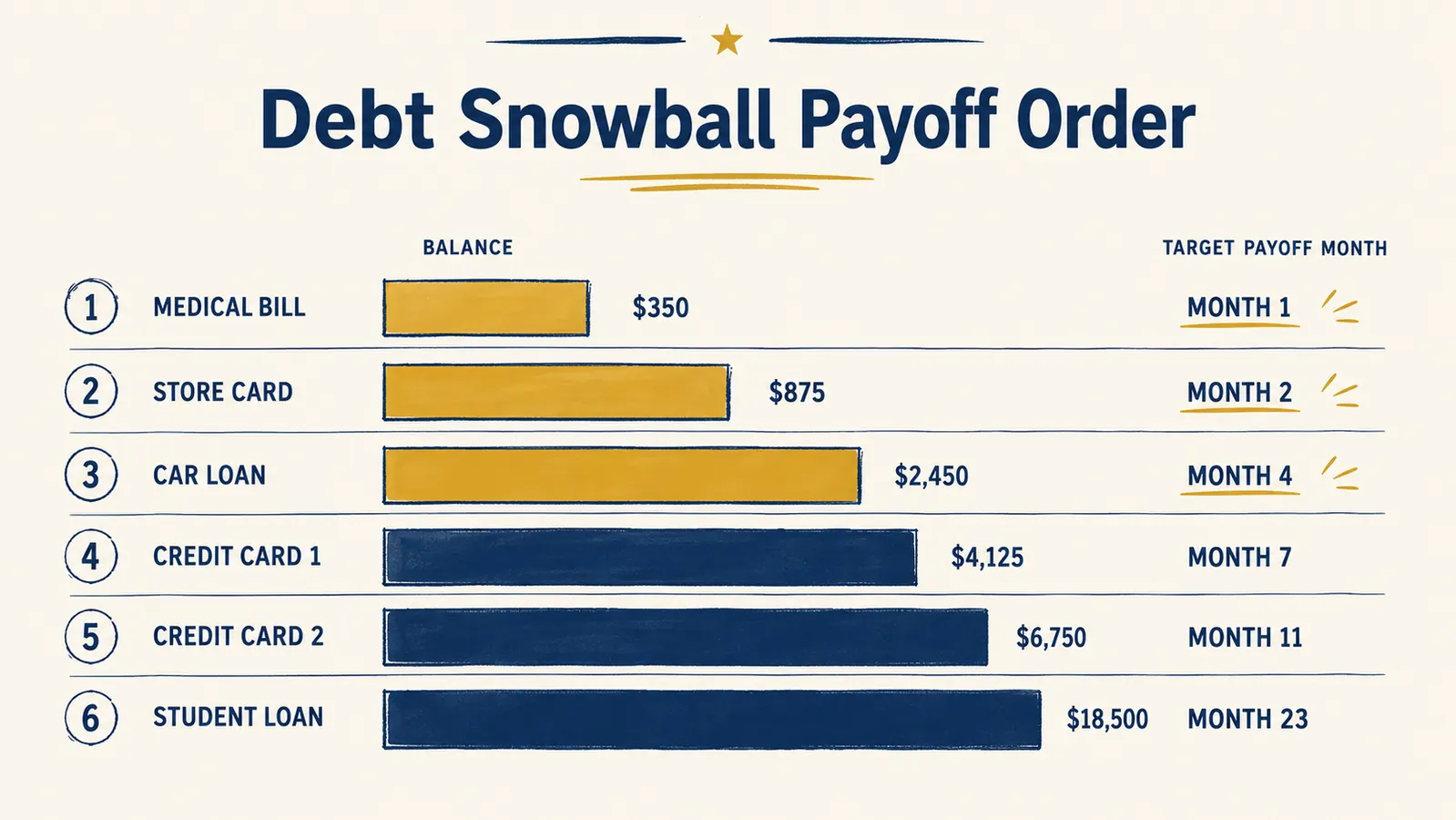

Step 3: Start the Debt Snowball (Baby Step 2)

This is the core of the Total Money Makeover and the step most people stay on for the longest time. The debt snowball works like this: you make minimum payments on every debt except the smallest one. On the smallest balance, you throw every extra dollar you can find. When that debt is paid off, you take the minimum payment you were making on it and add it to what you were paying on the next smallest debt. That is the snowball. The payment amount grows each time a debt disappears.

The reason the system orders debts by balance rather than by interest rate is psychological. Paying off a smaller debt fast gives you a real win early. That win builds momentum. People who follow the interest-rate-first method (called the debt avalanche) often burn out before they see results because the math takes longer to produce a visible payoff. Ramsey explicitly trades a small amount of mathematical efficiency for the emotional fuel to actually keep going. For most people, that trade is worth it.

My smallest debt when I started was a store card with a $640 balance. I paid it off in six weeks. That first paid-off statement hit different than I expected. It was only $640, but crossing it off my list made the rest of the plan feel real in a way it had not before. I moved that $40 minimum payment onto the next debt and started gaining real ground.

Step 4: Find Extra Money to Accelerate the Snowball

The debt snowball on minimum payments alone can take years. The way to shorten it significantly is to find extra money and funnel it directly at the smallest debt. The Total Money Makeover lists several approaches: selling things you do not use, cutting any non-essential subscription, working extra hours or a temporary second income, and temporarily pausing retirement contributions if you are not getting an employer match. These feel like sacrifices, and they are. Ramsey calls this stage gazelle intensity, borrowing a mental image of a gazelle running from a cheetah. Debt is the cheetah.

For me the most useful change was doing a real written budget for the first time. I had been mentally budgeting for years and had no idea where about $400 a month was going. When I wrote it out category by category, I found it in eating out, streaming services I had forgotten about, and a gym membership I had not used in eight months. Redirecting that $400 to my debt snowball cut my payoff timeline almost in half. Having the book nearby helped me stay connected to the why during the weeks it felt tedious.

Step 5: Stay Consistent Through the Boring Middle

The beginning of the debt payoff process has energy behind it because it is new. The end has energy because you can see the finish line. The middle is where most people slow down or stop. Balances are smaller but not gone. Life gets in the way. The starter emergency fund gets used and feels like a setback. This is normal. The Total Money Makeover prepares you for this by framing debt payoff not as a financial optimization but as a behavior change. It repeats the same principles multiple ways throughout the book precisely because humans need repetition to stay anchored to a plan.

The practical thing that helped me most during the middle stretch was keeping my debt list somewhere I would see it regularly. I kept a printed version on the inside of a kitchen cabinet door. Every time I crossed something off or updated a balance, I felt the progress. It sounds small, but visual tracking of a long-horizon goal matters more than most financial advice acknowledges. The debt snowball chart in the book is designed for this. Use it.

If you fall off the plan for a month, you restart the next month. You do not redo anything. You do not go back to square one. You pick up exactly where you left off. One bad month does not erase nine good ones. The Total Money Makeover is explicit about this because people quit from guilt more often than from genuine failure. The plan works. The only thing that stops it is stopping.

What Else Helps While You Work Through the Baby Steps

A physical budgeting tool makes the written budget from Step 4 much easier to maintain week to week. A lot of people who follow the Total Money Makeover system pair it with a cash envelope binder, which keeps spending in each category visible and physical. When the grocery envelope is empty, grocery spending stops for the week. There is no app that replicates that friction as effectively. If you want to look at options, the SKYDUE Budget Binder is one of the most popular choices for cash envelope budgeting and pairs naturally with what the Total Money Makeover teaches. You can find a full breakdown in our review of the SKYDUE Budget Binder.

The other thing worth doing while you are in Baby Step 2 is reading one chapter of the Total Money Makeover per week rather than all at once. The book is short enough to finish in a few sittings, but spacing it out keeps the principles fresh when motivation dips. I read it twice over the course of my payoff year. The second read landed differently because I had concrete experience to match against the advice. You will likely find the same.

Finally, do not skip straight to investing or homeownership while you still have consumer debt. The Total Money Makeover is specific about the order of the Baby Steps for a reason. Interest on credit card balances almost always outpaces what a beginning investor earns in a brokerage account. Finish the debt first, then build the three-to-six month emergency fund (Baby Step 3), then turn your full attention to retirement and wealth-building. The order matters. If you want to understand what comes after the debt payoff steps, our longer review of the Total Money Makeover covers the full arc of the Baby Steps and how each one builds on the last.

Writing down every debt I owed in one place was uncomfortable. But it stopped being a vague cloud of stress and became a specific number I could make a plan around. You cannot attack something you refuse to look at directly.

Ready to stop guessing and start crossing off debts? This is where it starts.

The Total Money Makeover walks you through every Baby Step with the context you need to actually finish each one. Rated 4.7 stars by more than 22,000 readers on Amazon. It is a short book, and it is one you will want to have in hand, not just read once on a screen.

Amazon Check Today's Price on Amazon →