I am Marcus. I am 41, I do HVAC service work out of Tulsa, Oklahoma, and I will tell you straight: I came to this binder as a skeptic. My wife Nicole had been talking about the cash envelope system for two years. I kept saying it sounded like something your grandmother did before ATMs existed. She finally ordered the SKYDUE Budget Binder in February without asking me, set it up on the kitchen counter, and told me to give it 60 days before I complained about it. That was eight months ago. This is not a love story about a binder. It is an honest account of what it actually does, what annoyed me, what surprised me, and who I think should buy it and who I think should skip it entirely.

The SKYDUE Budget Binder is a physical cash-envelope budgeting kit. You get a zippered A6 binder, clear zipper pouches in two sizes, preprinted category labels, monthly budget summary sheets, and expense log pages you fill in by hand. The concept is deliberate in its simplicity: pull cash out on payday, sort it into labeled envelopes by spending category, and when a pouch runs empty, you are done spending in that category until next pay period. There is no algorithm, no app sync, and no subscription. Just cash, paper, and the discipline of watching a physical supply run down.

The Quick Verdict

The SKYDUE binder does exactly what it promises for the categories where you can pay in cash. Its limitations are real and worth knowing before you buy, but for overspenders on groceries and dining out, the physical system beats digital willpower every time.

Amazon Check Today's Price →You have read about budgeting apps. You may have even downloaded a few. If they did not stick, the reason is probably that no app makes overspending feel real. This binder does.

Rated 4.7 stars by more than 19,000 buyers. See today's price on Amazon before you decide.

Amazon Check Today's Price on Amazon →How We Actually Use It

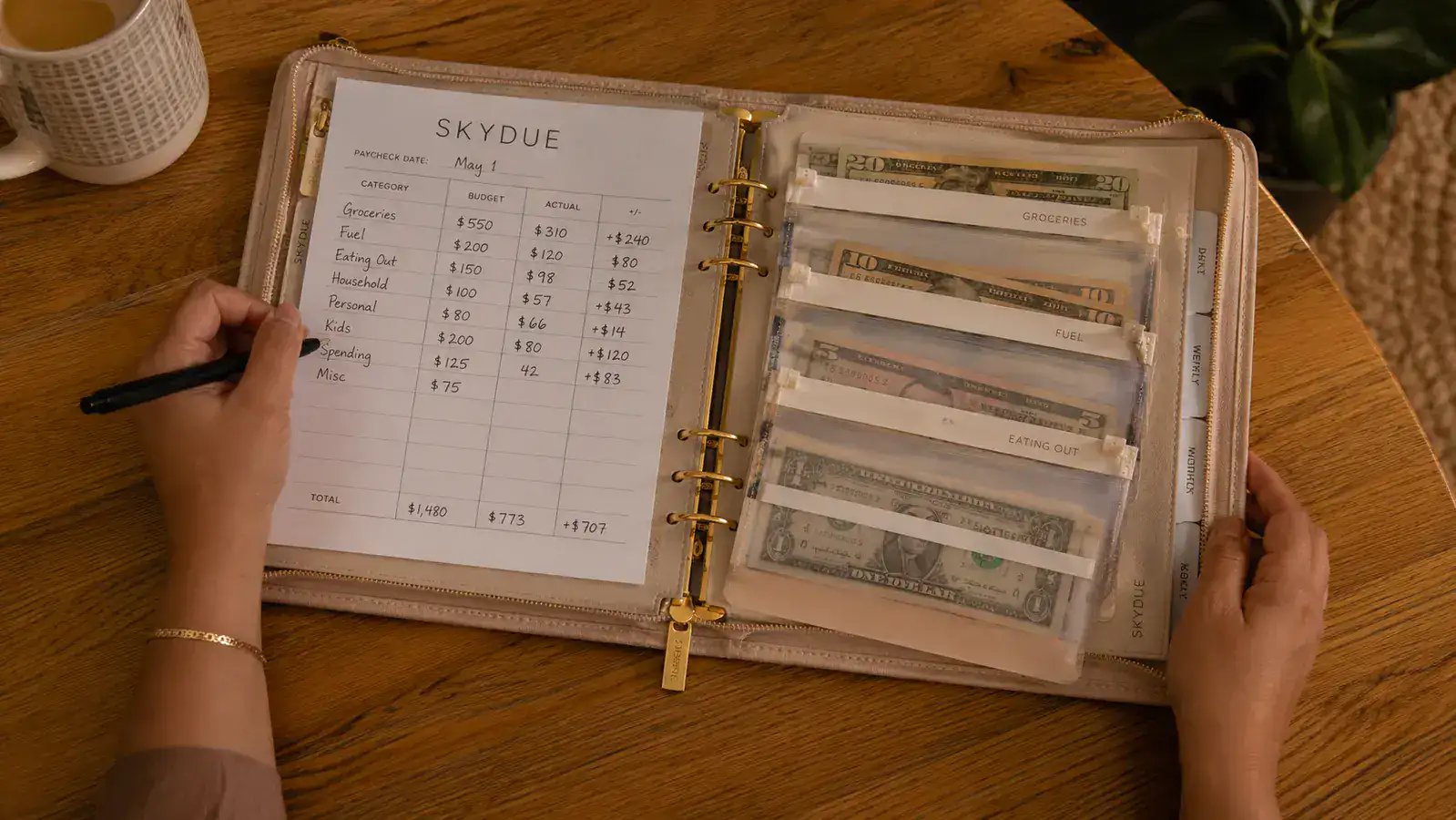

Nicole set up nine envelopes for us: Groceries, Gas, Eating Out, Household (cleaning supplies and paper goods), Kids' Expenses (our two boys, ages 9 and 13, have school fees and sports costs), Date Night, Pet (we have a beagle named Biscuit), Marcus Personal Spending, and Nicole Personal Spending. Those last two were her idea and they were smart. Each of us gets a small amount of personal cash every month to spend however we want, no questions asked. That eliminated about 80 percent of the budget arguments we used to have.

On the first of each month, Nicole goes to the bank, pulls the cash for all nine categories, and we sit together for about 25 minutes sorting and counting it into the envelopes. She fills in the starting balance on the expense tracking sheets. Then it runs on autopilot until the envelopes dictate otherwise. I carry my personal spending envelope in my wallet. The rest live in the binder on the kitchen counter. When I need cash from the Groceries envelope before a store run, I pull it from the binder. When I get change back, it goes back in.

That is the practical rhythm. It is not complicated. But there are things about this system that nobody tells you in the product listing, and I want to go through them honestly.

What the Five-Star Reviews Leave Out

First: envelope wear. The clear zipper pouches are not fragile, but they are also not indestructible. After eight months of daily handling, two of our pouches have small stress marks near the zipper teeth where the plastic flexes repeatedly. They have not torn. But if you are a rough handler, or you overstuff envelopes with coins and crumpled bills, expect to see some material fatigue by month six. Replacement pouches are available on Amazon, so it is not a dealbreaker, just something to know.

Second: the carrying-cash question. Eight months ago I would have said carrying cash feels outdated. I still think it has real security concerns that are worth naming. We keep the bulk of our monthly cash in the binder at home and only take out the specific envelope we need for a specific trip. That means if I lose my wallet, I lose my personal spending money but not the grocery budget for the whole month. If you carry the full binder everywhere, a theft or loss is a much bigger problem. Neither the product listing nor most reviews address this directly. You need to decide how you handle it, and building that habit takes a few weeks.

Third: the tracking sheet habit is harder than it looks. The sheets included in the binder ask you to log every transaction with a date, merchant, amount, and running balance. That is a great system in theory. In practice, on a Tuesday evening after a full day of service calls, I am not sitting down to log that I spent $7.40 on a car wash. Nicole does most of our logging and even she does it in batches every two or three days rather than in real time. That introduces small errors. The envelope still runs out when it runs out, so the hard limit holds. But the spending insight the tracking pages are designed to provide only works if you actually use them consistently.

The Part About What Cash Cannot Touch

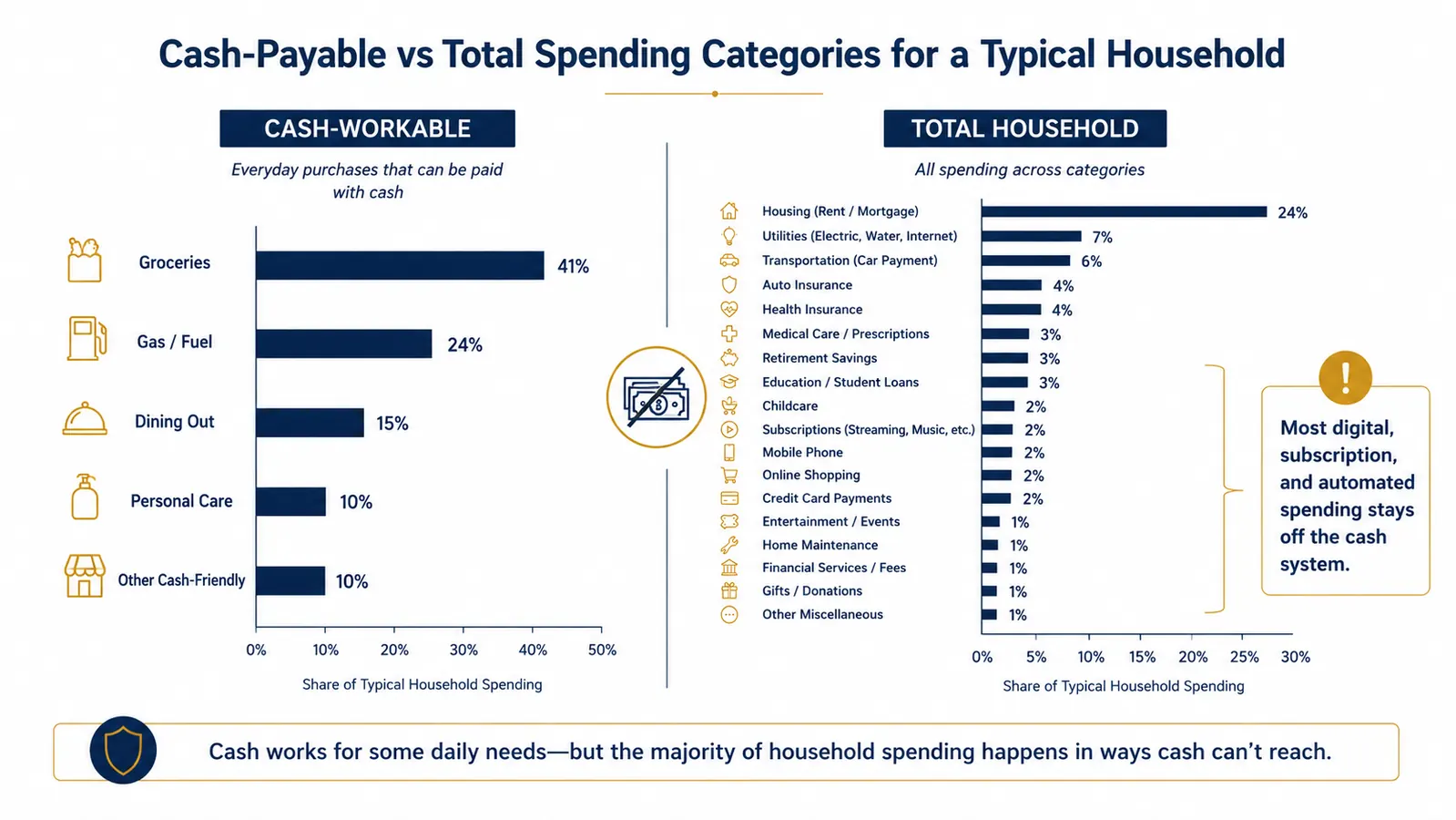

Here is the biggest honest limitation, and the one I think buyers need to sit with before purchasing. The cash envelope system only works for categories where you actually pay in cash. In our household, that realistically covers groceries, gas, eating out, and the date night fund. Our mortgage, both car payments, utilities, internet, streaming services, kids' school portals, the vet clinic that is only on card or check, and Amazon purchases all happen digitally. They are on autopay or charged to a credit card we pay off monthly. Envelopes do not touch any of that.

That is not a flaw in the SKYDUE binder specifically. It is a structural limitation of the cash envelope method in 2026. Before you buy, count how many of your actual overspending categories are payable in cash. If the answer is two or three, the binder can still help, but you should not expect it to transform your whole financial picture. It will sharpen your control over those specific categories and leave the rest of your spending to whatever system you currently have. For us, those two or three cash categories were exactly where we were hemorrhaging money, so it still moved the needle. Your situation may be different.

Nicole and I also pair the binder with a simple Google Sheet for our fixed expenses and debt payoff tracking. The binder handles variable cash spending. The sheet handles the rest. If you expect one physical product to replace all financial tracking, you will be disappointed. No single tool does that.

What Actually Changed for Us

I did not expect to have a lot to report on the positive side, given that I started skeptical. So let me be fair. In the month before Nicole bought the binder, we spent $740 on groceries for a family of four. Our first month with the binder, we budgeted $550 and spent $537. The next month, $519. By month four we were consistently landing between $490 and $520 and not feeling deprived. That is a reduction of roughly $200 per month on grocery spending alone. Over eight months, that is somewhere around $1,500 we did not spend on food that we would have spent before.

Our Eating Out envelope is set at $180 for the month. Before the binder, we had no idea what we were spending on restaurants and takeout. We looked it up in our bank statements when Nicole was setting up the system and it had been ranging from $290 to $420 per month. Not catastrophic, but consistently more than we would have guessed. Having a physical limit did not stop us from eating out. It just made us more deliberate about when.

I came in as the skeptic. Eight months later I am the one who refills the envelopes on the first of the month while Nicole handles the expense sheets. It did not change our income. It changed what we notice.

Build Quality: Honest Assessment After Eight Months

The binder cover is a soft faux-leather material with a snap closure. After eight months it still snaps cleanly and the material has not cracked or peeled. The carry handle is stitched on and still solid. The binder rings hold the tracking sheets without a problem. I did not expect this level of durability at the price point, and I want to say that plainly because my initial assumption was that it would feel cheap.

The zipper pouches, as I mentioned, show some surface wear by month six or seven with daily use. The zippers themselves still close properly. The clear plastic is thick enough to see your bills at a glance without opening the pouch, which is a practical detail that matters when you are in a parking lot checking if you have enough for the grocery run. The two sizes of pouches are a nice touch. The larger pouch works for the grocery and gas envelopes where you might have a heavier cash load. The smaller ones are fine for personal spending and date night where amounts are lower.

You will run out of the included expense tracking sheets. The binder comes with enough to get you through roughly two to three months depending on how many categories you run. Refill packs are sold separately on Amazon. Order them around month two and you will not hit a gap. I bought a refill pack around week ten and have been good since.

The Comparison Question Nobody Asks

People ask whether the binder is better than a budgeting app. That is the wrong comparison. An app can track your digital subscriptions, flag unusual charges, and show you a chart of your spending history across twelve months. The binder cannot do any of that. What the binder can do is make the physical act of overspending feel tangible and immediate in a way no app has managed. When the eating-out envelope is thin, you feel it in your hand. You do not feel it in an app. That difference sounds small. It is not small.

The right question is whether you are overspending in categories where you can realistically pay with cash. If yes, this binder will help. If most of your problem spending is online, on subscriptions, or on a rewards credit card you pay off monthly, the binder is solving the wrong problem for you. I lay out that comparison in detail in the SKYDUE binder versus YNAB comparison if you want the full side-by-side. For a broader look at what the binder gets right from a long-term use angle, the long-term SKYDUE Budget Binder review covers six months of consistent use with specific monthly numbers.

What I Liked

- Physical cash limit creates immediate, real-world spending accountability that apps cannot replicate

- Durable faux-leather cover and binder rings hold up well after months of regular handling

- Two pouch sizes included for high-load and low-load categories

- Personal spending envelopes per person eliminate budget arguments between partners

- Low cost of entry means you know within one month whether the system works for you

- Compact enough to keep on a kitchen counter without taking over the space

Where It Falls Short

- Zipper pouches show surface wear marks after six to eight months of daily use

- Only effective for cash-payable categories, which is a shrinking share of household spending in 2026

- Included expense tracking sheets run out in two to three months, requiring a separate refill purchase

- Carrying significant cash creates a security risk if the full binder leaves the house

- Tracking sheets require a consistent daily or near-daily habit to deliver meaningful spending insight

- No debt tracker, savings goal page, or income worksheet included

Who This Is For

This binder is the right call if you have tried at least one budgeting app and stopped using it within a few months. It is for people who can name two or three spending categories where they consistently go over and where cash is a realistic payment method. It is for couples who argue about discretionary spending and need a shared physical system both people can see and touch. It is for anyone who has ever opened a bank statement at the end of the month and genuinely not known where $300 went. At this price, the experiment cost is low enough that the question is not whether you can afford to try it. The question is whether you will actually engage with the system for 30 days and see what it shows you.

Who Should Skip It

Do not buy this binder if almost everything you spend money on is digital, automatic, or charged to a card for points. If your grocery delivery comes through an app, your gas goes on a fleet card through work, and your weekend spending is all tap-to-pay, cash envelopes will not touch any of it. The system needs friction to work, and friction only exists at the point of payment. Digital payments remove the friction entirely. Skip it also if you are looking for a complete financial management system in one product. It is not that. It handles variable cash spending and nothing else. If you need debt payoff tracking, investment monitoring, or bill management, you will need something else alongside it or instead of it. The binder is a targeted tool for a specific problem, and it works best when used by someone who is clear on which problem they are trying to solve.

If the real problem is that grocery and restaurant spending keeps running away from you, a physical envelope system will show you that clearly within the first 30 days.

Rated 4.7 stars by more than 19,000 buyers. Check today's price on Amazon and see what fits your budget categories.

Amazon Check Today's Price on Amazon →