For a long time, my 401k was just a number I tried not to look at too closely. I contributed enough to get the company match every year, which felt responsible, and then I left the rest alone because every time I logged in I felt like I was reading a menu in a language I did not speak. Growth funds, value funds, target-date funds, expense ratios. I had no idea what I was actually choosing, so I guessed. I clicked on whatever had the highest return in the little chart on the right side of the screen and hoped for the best.

That went on for about four years. Then a coworker of mine, Darnell, mentioned a book in passing during lunch. He said something like, 'I finally understand what I'm actually doing with my money. It's this short thing by the guy who invented index funds.' I wrote the title on a napkin and forgot about it for two months.

Eventually I ordered The Little Book of Common Sense Investing by John C. Bogle. It arrived in a small padded envelope and looked almost too thin to matter. Under 200 pages. I read the whole thing in two sittings over a weekend. By Sunday afternoon I had logged back into my 401k, and for the first time I actually understood what I was looking at.

For the first time in four years of contributing to a retirement account, I understood what I was actually paying for, and I understood why most of it was not working in my favor.

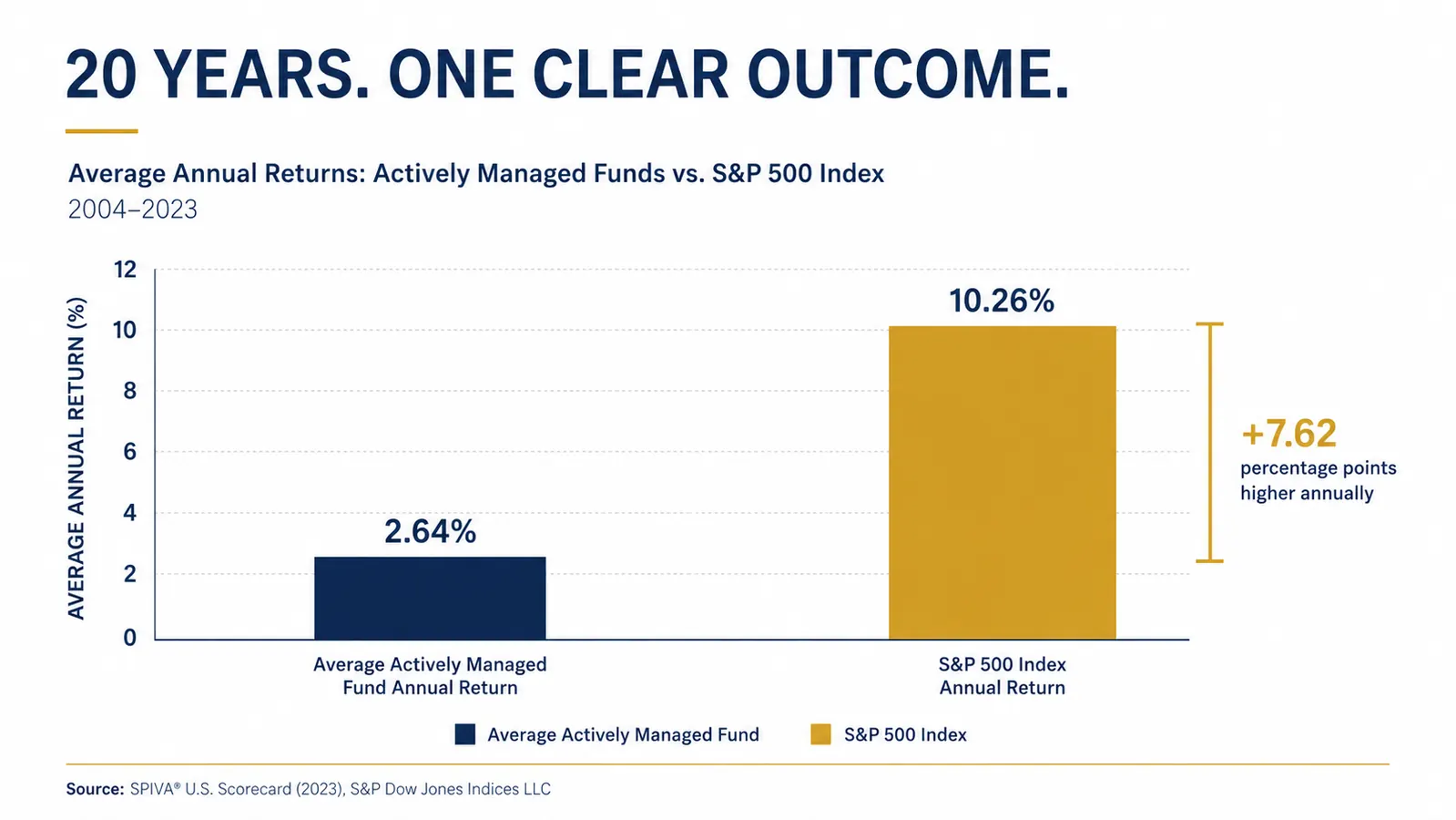

Bogle's core argument is not complicated. He says that over long periods of time, most actively managed mutual funds, the ones where a team of professionals picks stocks and charges you for it, fail to beat a simple index fund that just buys everything in the market at very low cost. He backs this up with decades of data. He also explains something I had never understood clearly before: every dollar you pay in fees is a dollar that does not compound. Over 30 years, that adds up to a number that will make your stomach hurt.

When I looked at my 401k allocation after reading that, I found two actively managed funds I had picked based on their recent performance charts. Both carried expense ratios above 1 percent. I had not thought much about those numbers before, but after reading Bogle's explanation I ran the math myself on a simple compound interest calculator. The difference between a 1.2 percent expense ratio and a 0.03 percent expense ratio, on contributions I planned to make over the next 25 years, was not small. It was the kind of number that is hard to ignore once you see it.

If your 401k feels like a guessing game, this is the book that changes that.

The Little Book of Common Sense Investing by John Bogle is short enough to read in a weekend and clear enough that you will actually understand it. It is the reason I finally stopped guessing and started making decisions I could explain.

Amazon Check Today's Price on Amazon →I want to be honest about something here. Reading Bogle's book did not turn me into an investing expert, and it did not dramatically change my account balance overnight. What it did was give me a simple framework I could actually trust. I moved a large portion of my 401k contributions into a low-cost total market index fund. I stopped trying to pick the best performer each quarter. I stopped watching financial YouTube channels that made me feel like I needed to be rebalancing my portfolio every other week. I just set up a consistent contribution and left it alone.

The psychological relief from that was something I did not expect. Investing had always felt like something I was probably doing wrong. After reading this book, I had a clear reason for the approach I was taking, and that reason was backed by a mountain of historical evidence, not a YouTube comment section. That is a different feeling entirely.

I also want to say that the book is not perfect. Bogle wrote it for a specific kind of reader and there are sections that feel repetitive, like he is making the same point four different ways. If you already have a solid grasp on how mutual funds work, some early chapters might feel slow. And the book does not spend much time on how to actually open an account or what to do if your 401k plan has limited options. For pure mechanics, you will want to pair it with something more hands-on, like a step-by-step beginner's guide to index funds. But as a foundation, as the thing that explains the why behind a simple investing approach, it is hard to beat.

What I'd Tell You If We Were Sitting at My Kitchen Table

If you are contributing to a 401k or a Roth IRA and you are mostly guessing, or if you have been meaning to start investing but the whole thing feels too complicated to begin, this is the book I would hand you. Not because it will make you rich. Not because it has some trading system or market prediction method. Because it will explain, in plain English, why simple works better than complicated when it comes to growing money over time, and it will give you the confidence to stop second-guessing yourself every time the market moves.

I paid less for this book than I spend on lunch most weeks. I read it once and have referenced it a handful of times since. The decisions I made after reading it are ones I am still comfortable with years later, which is more than I can say for anything I ever did based on a YouTube thumbnail. If you feel behind on retirement savings and you are not sure where to start making sense of it, start here.

Stop guessing and start understanding what your money is actually doing.

The Little Book of Common Sense Investing has over 11,000 reviews on Amazon for a reason. It is the clearest, most honest explanation of why index fund investing works, written by the person who made it possible. Check today's price and see if it is the starting point you have been looking for.

Amazon Check Today's Price on Amazon →