Three years ago I was sitting at my kitchen table with $18,400 spread across four credit cards, a car payment I could barely make, and the sinking feeling that I was going to be doing this for the rest of my life. I was 34, working a solid job as an office manager in Columbus, Ohio, making around $52,000 a year. On paper that sounds fine. In practice I was broke by the 20th of every month.

I had tried the envelope thing before. I had downloaded three different budget apps. I had a spreadsheet I built myself that I stopped updating after about six days. The problem was never knowing what to do. I could find a dozen articles telling me to "stop spending money on lattes," which, with all due respect, is not why people are buried in credit card debt. The problem was that I had no system. And more than that, I had no belief that a system could actually work for someone in my situation.

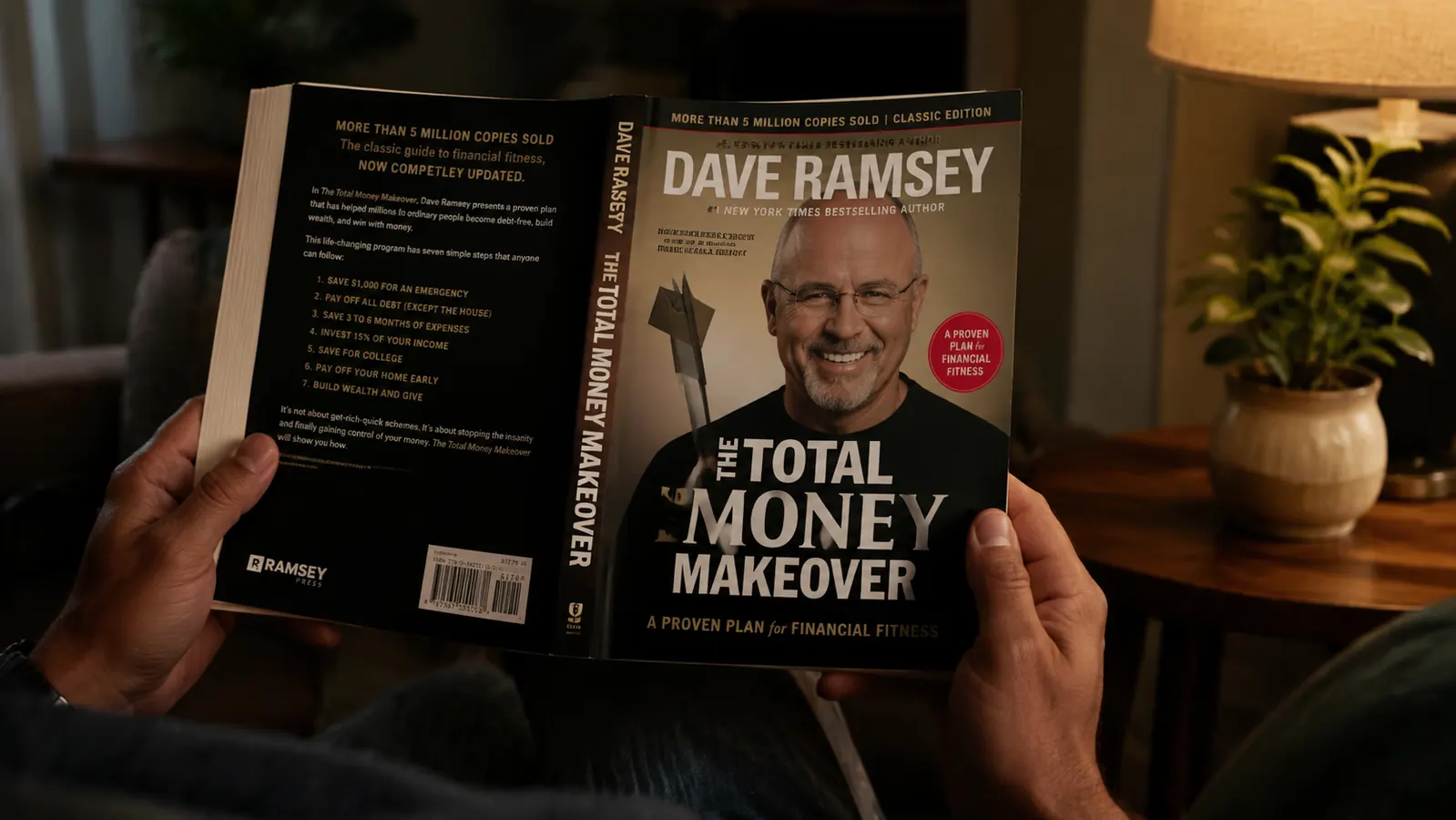

My sister-in-law Brenda changed that at Easter dinner in 2023, when she handed me a copy of The Total Money Makeover by Dave Ramsey. We were talking about money, the way you do when you think no one is listening, and she mentioned that she and her husband Marcus had paid off $27,000 in 22 months. I almost dropped my fork. They are not high earners. Marcus drives for a trucking company, Brenda works part-time at a school. I asked her what they did differently. She said, "We read a book and then we just did what it said." The book was The Total Money Makeover by Dave Ramsey.

I picked up a copy the following week. I expected it to feel like a lecture. It did not. Ramsey writes like someone who has been broke himself, because he has. He lost everything in his late 20s and spent years figuring out what actually works for regular people. The book is structured around seven baby steps, and the first three are entirely focused on stopping the bleeding before you worry about anything else. Step one: save a $1,000 starter emergency fund. Step two: attack your debts smallest to largest using what he calls the debt snowball. Step three: build a three-to-six month fully funded emergency fund before you touch investing.

I had heard of the debt snowball before and dismissed it as mathematically inefficient. Technically you should pay off the highest interest debt first. Ramsey openly admits the snowball is not optimized for math. It is optimized for human behavior. You pay off the smallest balance first, feel the win, and use that momentum to attack the next one. I thought that sounded like a trick. Then I actually tried it.

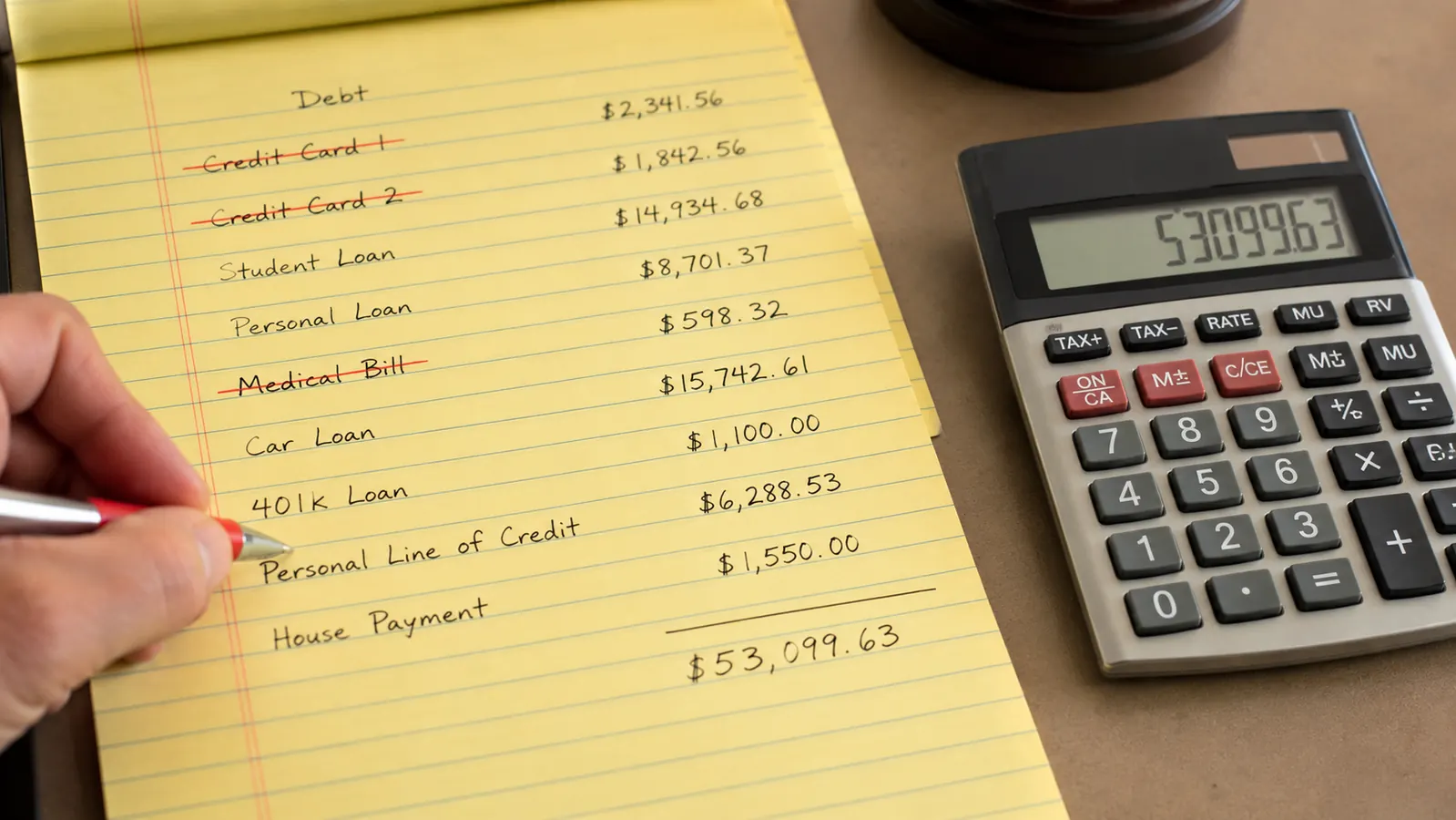

I paid off my smallest card, a $640 store card, in 47 days. That one small win did more for my mindset than three years of spreadsheets.

My smallest balance was $640 on a store card I had opened for a discount and then forgotten about. I threw every spare dollar at it for 47 days and cleared it. That sounds trivial. But crossing it off my list did something to me that I cannot fully explain. It felt real in a way that all my previous budgeting attempts had not. I wrote the zero down with a red pen and taped it to the inside of a kitchen cabinet. My husband thought I was losing it. Two months later he was asking me when we were going to hit the next one.

The book that actually explained why I was stuck, and what to do about it

The Total Money Makeover by Dave Ramsey has over 22,000 reviews on Amazon for a reason. It is not about motivation. It is a step-by-step system written for people who have already tried the vague advice and want something concrete. If you are carrying credit card debt and feel like you are running in place, this is the first book I would hand you.

Amazon Check Today's Price on Amazon →We cleared the full $18,400 in 19 months. I am not going to pretend it was easy or that we never argued about money during that stretch. We ate a lot of meals at home. We canceled subscriptions. We had one real vacation in those 19 months, a long weekend in Hocking Hills that cost us $340 total. The book does not promise you will enjoy every part of this. What it promises is that the system works if you work the system. That turned out to be true.

There are things the book does not cover that I had to figure out on my own. It does not talk much about navigating debt when your income is irregular, which is something gig workers and freelancers run into immediately. And the investing chapters in the later baby steps are written at a fairly surface level. If investing is your main focus, you will want to supplement with something like The Little Book of Common Sense Investing once you get there. But for people in the debt stage, which is most people who feel behind, this book is precisely calibrated to that problem.

There is also a real tension in Ramsey's approach around credit cards specifically. He argues for cutting them up entirely, which is more aggressive than a lot of financial advisors recommend. I did not cut mine up. I froze them, which I later learned is a common compromise people make. The underlying principle, which is that you cannot manage debt you keep adding to, is still sound. You can adapt the tactics to your situation.

What I'd Tell You If We Were Sitting at My Kitchen Table

Here is what I would actually say to you, friend to friend, not blogger to reader. If you are carrying credit card debt and your budget keeps falling apart, you do not have a discipline problem. You have a system problem. Nobody can hold a leaky bucket together through willpower. You need a structure that makes the right move the obvious move, and that is what this book gives you.

You do not have to agree with everything Ramsey says. I do not. But the debt snowball method is real, and it works on a psychological level that purely math-based plans often miss. If Brenda and Marcus can clear $27,000 on a combined income that most people would not brag about, and I can clear $18,400 on a single middle-income salary, the system is not the variable. The variable is whether you actually start.

Pick up the book. Read the first three baby steps. Do not skip ahead. Do not wait until the timing is better, because the timing never gets better on its own. If you want to go deeper on the actual debt payoff mechanics before you dive in, I have a full walkthrough of how to apply the method step by step over at how to pay off debt with the Total Money Makeover. And if you want the longer, more detailed take on the book itself, my six-month review covers what held up and what surprised me. But honestly, the best next step is just to get the book in your hands.

Ready to stop running in place? This is the starting line.

The Total Money Makeover is the book I wish someone had put in my hands five years earlier. Rated 4.7 stars across more than 22,000 Amazon reviews. Read it, follow the steps, and come back in six months to tell me how it went.

Amazon Check Today's Price on Amazon →